The Federal Employee Retention Tax Credit (ERTC) offers eligible employers significant tax benefits through an ability to claim a refundable tax credit for paying qualified wages and certain health plan expenses. Employers may be able to receive as much as $33,000 per employee in incentives.

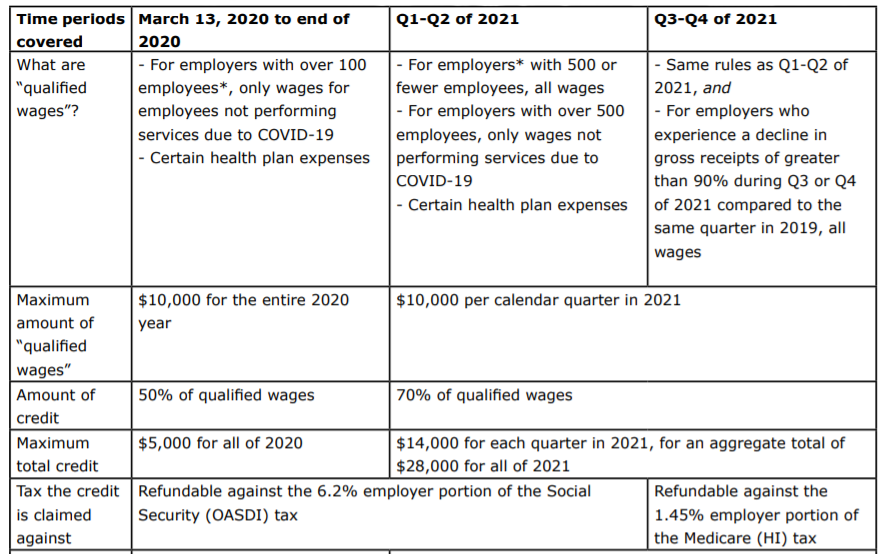

The American Rescue Plan Act (ARPA) extends the ERTC through the end of 2021. There are different rules for the treatment of wages employers (1) paid from March 12, 2020 through December 31, 2020; (2) pay in the first half of 2021; and (3) pay in the second half of 2021 (the IRS guidance for the 2021 ERTC has not yet been issued).

Eligibility for the tax benefits is also linked to an employer’s size, the impact of the pandemic on an employer’s ability to provide services, and the suspension of operations because of government mandates or reductions in quarterly gross receipts.

Employers can receive both Paycheck Protection Plan (PPP) loans and claim ERTC benefits, but there are limits on “double-dipping” (the eligible employer can claim the ERTC on any qualified wages that are not counted as payroll costs in obtaining PPP loan forgiveness). ARPA also makes the ERTC available to “recovery start-up businesses” that began carrying on a trade or business after February 15, 2020, and that have annual gross receipts of $1 million or less.

ARPA Available Employer Tax Credit Incentives

If you are an employer with a question about the ARPA, contact Tracy Armstrong or another member of the Wilentz Employment Law team.

Tags: Coronavirus (COVID-19) • Families First Coronavirus Response Act (FFRCA) • American Rescue Act of 2021 • Paycheck Protection Program • Employee Retention Tax Act